Key Points

- A One-Time Close (OTC) loan wraps land, construction, and permanent mortgage into a single closing—saving duplicate closing costs.

- Most standard lenders won’t fund modular factories before the unit ships; you need a modular-experienced lender.

- Modular builds complete in 3–5 months vs. 12–18 for stick-built, cutting construction loan interest significantly.

- FHA, VA, USDA, and Conventional loan products all support One-Time Close construction loans for modular homes.

- When calling lenders, ask specifically about ‘off-site materials draws’—this is the key modular financing question.

Financing Your Prefab Project: Construction Loans, Draws, and the One-Time Close

Sarah walked into her Wells Fargo branch excited. She'd found the perfect modular home builder in Colorado—efficient design, move-in ready in four months, price that didn't require a second mortgage. But when she mentioned the factory deposit to the loan officer, the conversation died. "The factory needs 30% down before they start building," she said. The officer squinted at his computer. "That's not on-site construction. We can't release funds for materials not on your property. That violates our draw schedule guidelines." Sarah's stomach sank. She'd been pre-approved for a conventional mortgage, but her lender had no mechanism for the factory draw. Two weeks later, she nearly lost her factory slot.

This happens more often than you'd think. Regular mortgage lenders—the big banks, the chains you see on every corner—weren't built to finance modular homes. Their underwriting systems assume stick-built construction, with funds released at each on-site inspection milestone. Factory deposits? Draw schedules for off-site materials? It doesn't compute.

But here's the good news: the financing structure exists. You just need to find the right lender. And when you do, you'll save money in ways stick-built buyers never will.

What Is a One-Time Close Construction Loan?

A one-time close construction loan (often called an OTC loan) rolls everything into a single closing: land purchase, construction financing, and permanent mortgage. You close once, not twice.

Here's why that matters for your wallet. Traditional construction financing works like this: you close on land, then close again when construction is done and the bank converts the construction loan to a permanent mortgage. That's two separate closing events. Duplicate title searches ($500-$800), duplicate appraisals ($500-$800), duplicate attorney fees, duplicate recording costs. You're looking at $5,000 to $15,000 in redundant closing costs. With an OTC loan, you skip that second closing entirely. You close once on the combined loan amount and walk out with a permanent mortgage already in place.

These loans come in four flavors: Conventional, FHA, VA, and USDA.

Conventional OTC loans typically require 10-20% down and good credit (680+). They're the fastest to close and offer the most flexibility on lender choice.

FHA one-time close loans require only 3.5% down and accept credit scores as low as 580. The catch: your modular home must be built on a permanent foundation (not a temporary frame), and it has to meet HUD's permanent installation standards. Colorado's Elevations Credit Union has done dozens of FHA modular builds and understands exactly what HUD requires.

VA loans work similarly to FHA—no money down if you're eligible, faster approvals for veterans than traditional VA construction financing.

USDA loans apply in rural areas, which is perfect for modular. If you're building in rural Fremont County, Custer County, or the eastern plains, a USDA OTC loan might be your cheapest option.

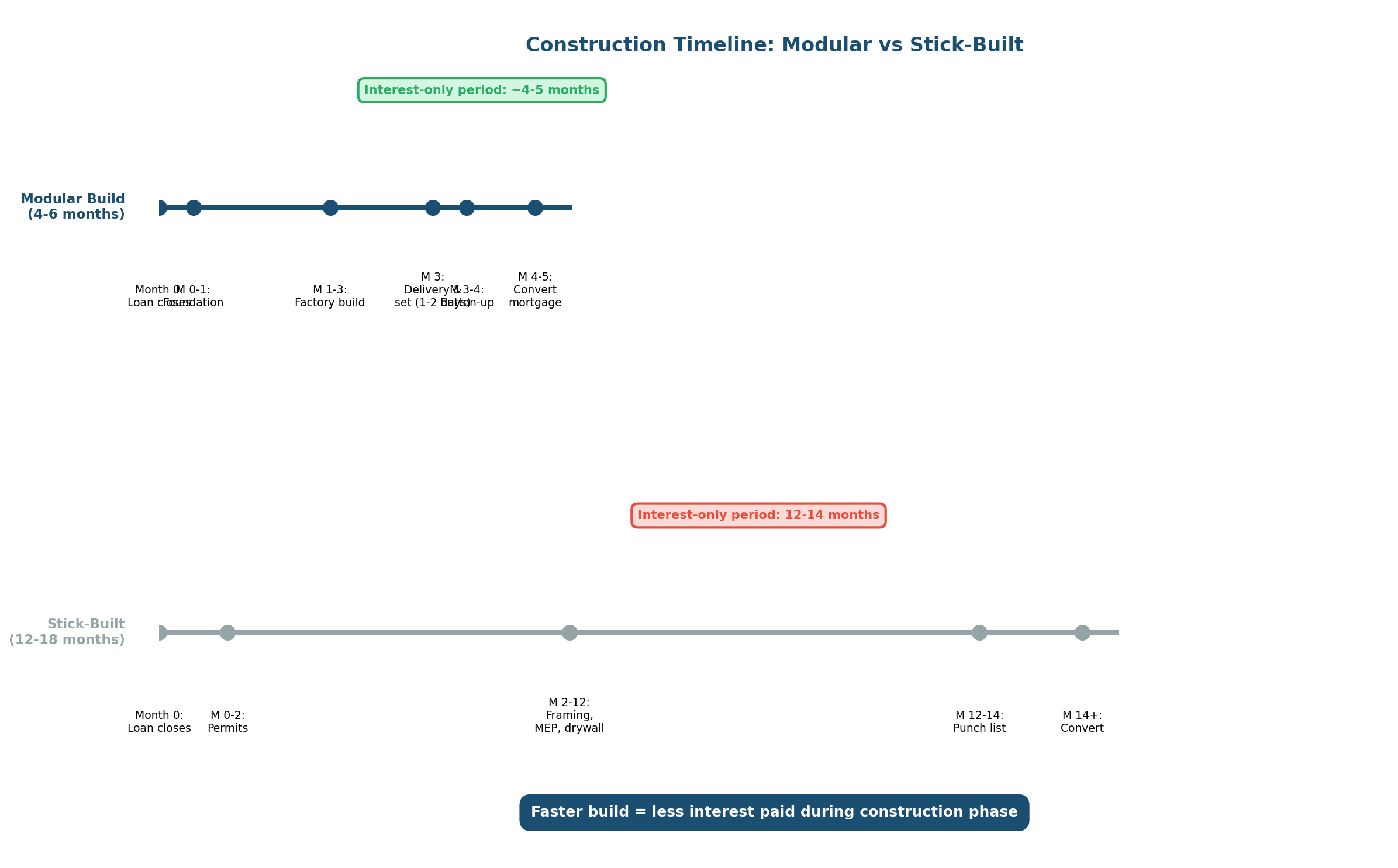

During the construction phase (typically six to twelve months for traditional builds, but only three to four months for modular), you make interest-only payments on whatever funds have been drawn from the loan. You're not paying down principal yet—just financing the borrowed money while work happens.

The Draw Schedule Problem (And How to Solve It)

This is where modular financing gets tricky.

Traditional construction lenders have a completely legitimate system: they release money as work is completed on-site. First draw at framing inspection. Second draw at drywall inspection. Third draw at electrical rough-in. Each milestone means visible, verifiable progress. The lender sends an inspector to the property. They confirm work is done. They release the next tranche. It's safe. It's predictable. It's designed for stick-built homes.

Modular homes break this model in half.

Your modular factory doesn't build piece-by-piece to your on-site timeline. They're building dozens of homes simultaneously, in assembly-line fashion. They need 20 to 50% of the total build cost upfront—before your modules even enter the factory floor. They need it to buy materials for your specific home, set up production slots, reserve skilled labor. No deposit, no factory slot. Your home goes to the back of the queue.

But here's the problem: traditional lenders see "release funds for work not happening on the property" and their compliance systems reject it. Their underwriting manual says funds must be released against visible progress on-site. Off-site factory builds don't fit the template.

So you end up in Sarah's situation: pre-approved for a loan you can't actually use.

The solution is finding lenders who specialize in modular construction and have explicit draw-schedule provisions for factory advances.

Capital Home Mortgage in Colorado handles this routinely. They've financed dozens of modular projects. When they set up your draw schedule, they build in factory deposits. They don't need an on-site inspection for factory payment—they release funds against a factory invoice and a financial review of the manufacturer. Many modular builders carry performance bonds, which gives the lender additional security.

Elevations Credit Union operates the same way. They're in Boulder, but they serve members across Colorado. They've built out specific protocols for modular factory draws because they've seen the pain point. Your FSB, based in Missouri but operating in Colorado, also has modular-ready construction financing.

What do these lenders require to release factory funds? Typically:

A detailed factory invoice tied to your specific home (not just a generic cost estimate)

Current financial statements from the manufacturer proving solvency

A copy of the builder's contract, showing the factory draw timeline

Sometimes a performance bond from the manufacturer (varies by lender)

That's it. No on-site inspection for factory draws. They understand the modular pipeline.

This is worth asking about directly when you're shopping lenders. "Do you have experience with modular factory draws?" If they look confused, keep looking.

Interest-Only Payments and the Speed Advantage

Here's where modular homes win a brutal math battle against stick-built.

Let's say you're borrowing $250,000 at 7% interest on a construction loan.

If you're building stick-built and construction takes 12 months (realistic timeline: site prep, foundation, framing, mechanical, drywall, finishing), you're paying interest-only for a full year. That's roughly $1,458 a month in pure interest. Twelve months at $1,458 = $17,500 in interest before you own a completed home.

Now imagine your modular build takes four months. Factory construction is three to four months, then delivery and on-site assembly is another one to two weeks. Your interest-only period is just four months. That's $5,833 in total interest payments.

You just saved $11,667. Before the first trade even showed up at your property.

That savings doesn't come from a different lender or a lower interest rate. It comes from the physics of modular construction. Faster build time equals less interest paid. The clock stops ticking faster.

This is the hidden win in modular financing. It's not just about monthly savings after you close. It's about thousands in interest you don't pay while waiting for the home to be finished.

What About FHA, VA, and USDA for Modular?

Misconception time.

Myth: "FHA doesn't finance modular homes."

Reality: FHA absolutely finances modular homes. The requirement is that your modular home sits on a permanent foundation (not a mobile home frame) and meets HUD's permanent installation standards. If your home meets those two conditions, FHA will back an OTC loan. Elevations Credit Union in Boulder has FHA modular closings regularly.

Myth: "VA loans only work for stick-built."

Reality: VA loans work for modular the same way they work for site-built. You need a permanent foundation, full-residency intent, and a lender willing to do the paperwork (not all do). But you're eligible. No down payment required if you're qualified. And the VA will back the OTC structure.

Myth: "USDA loans aren't available in Colorado."

Reality: USDA loans are available in rural Colorado. If you're building in rural areas—Fremont County, Custer County, Teller County, or anywhere outside the Denver metro that USDA designates as rural—you're eligible for a USDA guaranteed construction loan. USDA loans often have the lowest interest rates of any federal program, and they don't require a down payment. For rural modular projects, they're money.

The key across all three programs: find a lender who has experience with modular, understands the OTC structure, and won't panic when they see a factory deposit on the draw schedule.

Back to Sarah.

After her Wells Fargo rejection, she called Capital Home Mortgage. She explained the scenario: modular home, factory deposit upfront, 30-day factory timeline before on-site construction. The loan officer asked a few clarifying questions and said, "This is totally doable. Here's what we need for the factory draw."

Sarah gathered the documents in three days. The lender reviewed them and approved the factory draw provision in 10 days. She closed on the OTC construction loan without losing her factory slot.

The financing detail that nearly derailed her entire project? Solved. The lender mattered as much as the builder.

That's the lesson. Your regular bank, the one you've had a checking account with for ten years, probably can't handle modular construction financing. They'll try. Their systems will fight them. You'll wait for phone calls that take weeks. Don't go there.

Find a lender in the Colorado modular ecosystem. Capital Home Mortgage. Elevations Credit Union. Your FSB. These firms have built the systems, the protocols, and the draw schedules specifically for this situation. They close faster. They understand factory deposits. They know the modular build timeline.

You'll close your OTC loan, lock in your permanent rate, and save thousands in interest while your home is being built.

That's worth the phone call.

To understand the full cost picture before you finance, check out our guide: The Ultimate Guide to Buying a Modular Home and ADU in Colorado.

Frequently Asked Questions

What is a One-Time Close construction loan?

A One-Time Close (OTC) loan combines land purchase, construction financing, and permanent mortgage into a single closing—saving duplicate closing costs and locking in your permanent rate before construction begins.

Why do I need a special lender for modular construction?

Modular factories require deposits before shipping—often 10–50% of unit cost. Standard construction loans only fund completed on-site work, so you need a lender comfortable releasing funds for off-site materials.

Can I use an FHA loan for a modular home?

Yes. FHA, VA, USDA, and conventional loans all offer One-Time Close construction products for modular homes placed on permanent foundations.