Key Points

- Modular homes use the International Residential Code (IRC)—identical to the standard for site-built homes.

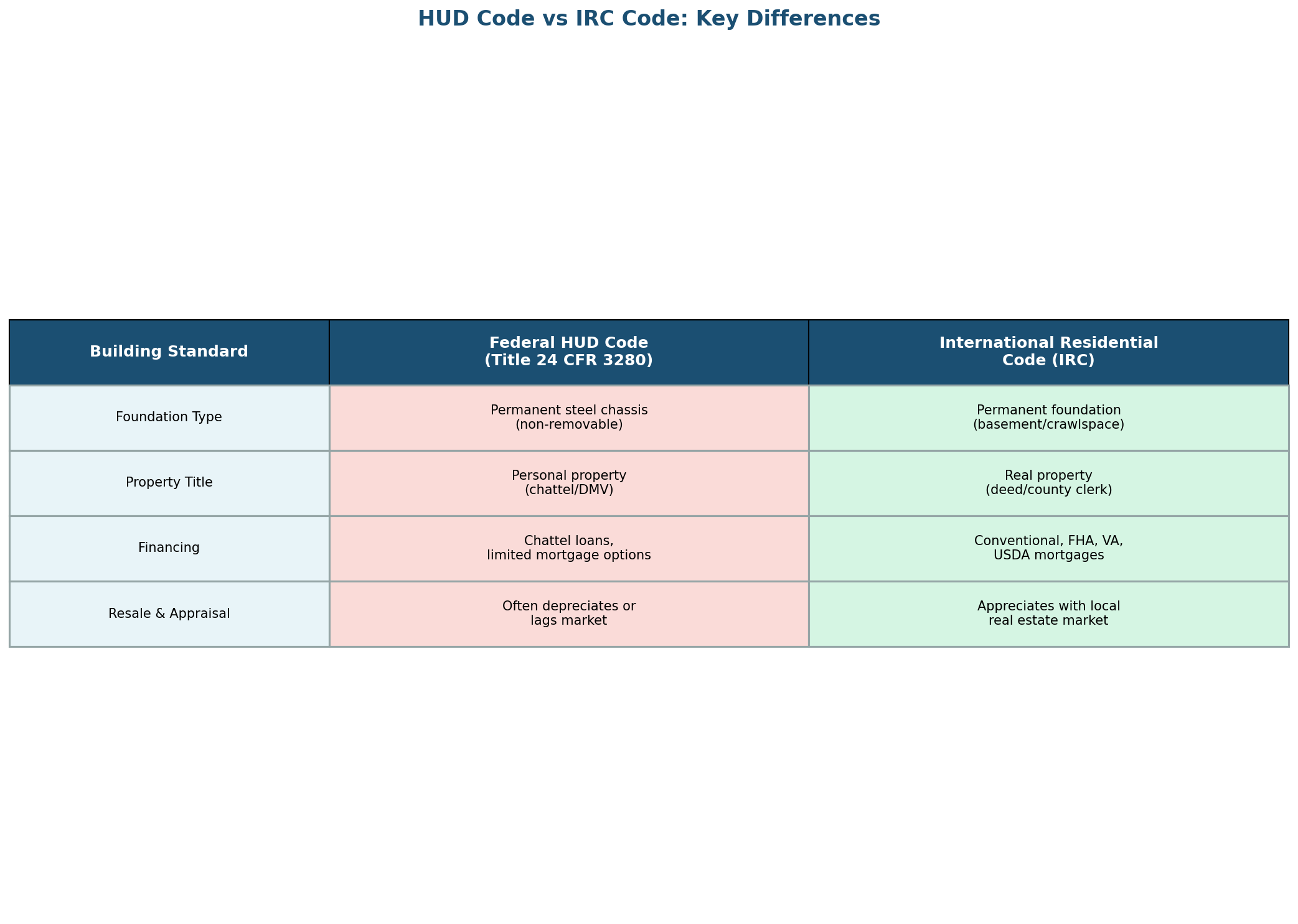

- Manufactured homes use the federal HUD Code and are often titled through the DMV as personal property, not real estate.

- Banks finance modular homes with conventional, FHA, VA, and USDA mortgages—the same products as site-built.

- Modular units contain up to 30% more lumber than stick-built, a transport engineering requirement that becomes a durability advantage in Colorado’s high winds.

- Once on a permanent foundation, modular homes appreciate alongside the local real estate market with no ‘modular discount.’

You're ready to buy. You've found a stunning modular home with everything you want — energy-efficient, beautiful finishes, priced right. You call your bank to get pre-approved for financing, and the loan officer asks: "Is this a manufactured home?" You say no, it's modular. There's silence. Then: "We can't finance manufactured homes. You'll need to look elsewhere."

Thirty seconds of confusion just cost you thousands of dollars and months of complications.

This happens constantly. And it shouldn't. The conflation of "modular" with "manufactured" homes is creating real financial and legal consequences for buyers, especially in Colorado where zoning codes are strict and local inspections are rigorous. Banks reject applications. Municipalities deny permits. Appraisers undervalue properties. All because the three housing types — modular, manufactured, and site-built — look superficially similar but operate under completely different regulatory frameworks.

Here's the thing: they're not the same. Not even close.

The Legal and Code Difference — HUD vs. IRC

The most critical distinction lives in the building code. It determines everything else: where you can build, how you finance it, what it's worth, and whether a conventional mortgage even exists.

Modular homes follow the International Residential Code (IRC) — the exact same code that governs traditional site-built homes. They're inspected at the factory, then again on-site after assembly. Colorado's Department of Housing (DOH) reviews factory-built modular plans and stamps them with approval. Local building departments conduct final inspections just like they would for any stick-built house. You can check the full process at the Colorado DOH factory-built structures page.

Manufactured homes, by contrast, are built under the federal HUD Code (Title 24 CFR 3280). This is a different standard entirely. It overrides local zoning codes and building amendments. A manufactured home that passes HUD inspection doesn't need to pass Colorado's local IRC amendments, which can be strict. Colorado municipalities enforce rigorous IRC amendments for snow loads (especially in mountain counties like Clear Creek and Summit) and wind shear resistance.

For Colorado buyers, this distinction has teeth. Many single-family residential (SFR) zoning districts explicitly prohibit HUD-code homes. Why? Because HUD code is a federal floor, not a ceiling. A manufactured home approved in Texas might not meet Colorado's snow load requirements. Local jurisdictions can't modify HUD code compliance — it's federal law. So they just ban the entire category.

The physical difference is also stark. Manufactured homes are built on a permanent non-removable steel chassis. They come with wheels and a hitch. Modular units, by contrast, are placed on a permanent foundation — a basement, crawlspace, or pier-and-beam system. Once the modular home is positioned and the utility connections are made, you remove the temporary support beams. The house is now part of the real property.

Foundation, Transport, and the 30% Rule

Here's something most people don't know: modular homes are engineered to withstand highway transport at 65 mph plus the stress of crane lifting during installation. This requirement drives up the structural complexity in ways that stick-built homes never experience.

To survive that journey, modular units use approximately 30% more lumber than a comparable site-built home. The framing is reinforced. Drywall is glued and screwed instead of nailed. Interior walls are thicker to handle the flexing that occurs during transport. Corner posts and load-bearing components are engineered with extra capacity.

This accidental over-engineering has a surprising benefit in Colorado. Wind speeds here can exceed 115 mph, especially in mountain passes and on exposed ridges. The Front Range regularly sees wind gusts over 70 mph. That extra structural rigidity — the thing that keeps a modular home from shaking apart during highway transport — translates directly into superior wind resistance.

You're paying for an engineered structure that's already proven it can handle extreme dynamic forces. When a microburst hits your valley, your modular home's reinforced framing is absorbing those loads better than a site-built home engineered to the bare minimum IRC requirements.

The transport engineering also means better quality control. A site-built home is assembled once, on-site, with different crews and different suppliers. A modular home is built in a factory by the same crews, using the same materials, every single time. If the roof connection detail doesn't work, the factory catches it on unit one. They don't build 500 more homes with the same mistake.

Financing and Long-Term Appraisal Value

This is where the rubber meets the road. Modular homes are real property. Manufactured homes are chattel.

When you finance a modular home, the lender is securing a mortgage against real estate — the same legal instrument used for any site-built house. You get a traditional 30-year mortgage, conventional rates, and conventional terms. After you build, you refinance out of the construction loan into a permanent mortgage. You build equity. You pay down principal. When you sell, you realize that equity as capital gain (or loss, depending on the market).

Manufactured homes are typically titled through your state's DMV as personal property — like a vehicle. The "home" itself is personal property; the land might be real property if you own it. But the financing is different. You're getting a chattel loan, not a mortgage. The term is typically shorter. The rates are higher. The lender's legal claim is weaker. And if you want to sell, you need to transfer the title through the DMV, not a deed.

This personal property vs. real property distinction creates a massive ripple effect.

When you refinance your modular home five years from now and that property appraiser walks through, they're treating it identically to the stick-built home two streets over. They're pulling comp sales from the neighborhood. They're checking the local market trends. They're appraising based on real estate dynamics.

With a manufactured home? The appraiser is often stumped. Comp sales for chattel homes are sparse in most markets. The appraisal methodology breaks down. Even if the home itself is newer and nicer than the site-built comp, the legal category creates friction.

Colorado doesn't have a huge inventory of HUD-code homes in SFR zones, so appraisers here are often working without local data. They fall back on conservative valuations. Even a pristine manufactured home might appraise lower than a comparable site-built home simply because the comp sales data doesn't exist.

Now, there's recent research worth noting. The Urban Institute published analysis showing that modern manufactured homes — units with pitched roofs, garages, and higher-end finishes (sometimes called CrossMod or "luxury" manufactured) — can appreciate similarly to site-built homes over time. You can read the full findings at the Urban Institute's research on manufactured home appreciation.

But here's the catch: that's recent data. The stigma in appraisal practices is older. Many appraisers and lenders still operate under the assumption that manufactured homes depreciate. That bias is slower to change than the reality.

With a modular home, you don't have that headwind. Once your modular home is complete and the final inspection is signed off, it's registered as real property. The title office records it as real estate. When an appraiser shows up, they're pulling comp sales from the neighborhood and local market — the same dataset they'd use for any stick-built home. Your modular home appreciates in lockstep with the local real estate market. In Denver or Boulder or Fort Collins, if the neighborhood appreciates 4% annually, so does your modular home.

And when you want to refinance or sell, that equity is treated like equity. You can pull it out. You can build on it. You can use it as collateral for other projects.

For Colorado buyers planning to stay in-state and build long-term wealth through real estate, this is the difference between a home that's legally attached to your financial future and one that's not.

The path forward is clearer than you think. You're not dealing with a trailer. You're dealing with a home engineered to IRC standards, built to handle extreme transport stress, financed as real property, and appraised alongside the rest of your neighborhood.

When your bank asks "Is this a manufactured home?" you can say no with confidence. And you can cite the code. You can reference the Colorado DOH inspection process. You can show the IRC compliance. The confusion isn't your fault — but knowing the difference means you're never caught off guard again.

For the full picture on modular costs, financing, and Colorado ADU law, read our complete guide: The Ultimate Guide to Buying a Modular Home and ADU in Colorado.

Frequently Asked Questions

Can a manufactured home be converted to real property?

Yes, through a process called title elimination, but appraisal stigma can persist. Modular homes on permanent foundations avoid this issue entirely.

Do modular homes appreciate in value?

Yes. Once permitted and placed on a permanent foundation, modular homes appreciate at the same rate as comparable site-built homes in the same market.

Can I get a regular mortgage for a modular home?

Yes. Modular homes qualify for conventional, FHA, VA, and USDA mortgages—the same products used for traditional site-built homes.